The traders dealing in the textile business got relief from the hike of Goods and Services Tax. The GST council has decided to put the provision, to increase the rates of tax on specific garments, on hold for some time. The council said that they have decided to keep the GST rate fixed to 5% on the garments costing below INR 10,000. The council had previously given indications that they might remove the 5% tax slab for garments and charge a tax at the rate of 12% instead.

Knitwear Club finance secretary Harish Kairpal said that the traders of the club were thankful to the council for making the decision. He said that the hike would have destroyed the manufacturers who were already struggling with the drop in demands from both domestic and international markets. He also urged the government to introduce the required reforms for the manufacturers to face the recession.

Atul Saggar, general secretary of Apparel Manufacturers Association of Ludhiana, said that the decision taken by the council was a big relief for the manufacturers as the 7% hike in the taxes would have increased the cost at a time where they already are facing a shortage of orders.

Sukhvinder Singh, a garment manufacturer, and a member of the Ludhiana Business Forum said, “The currently applicable GST of 5% on certain fabrics and garments costing up to Rs 1,000 is already non- refundable, and when the same rate is into force for more than three years now, why did the government want to change it now. The stand taken by GST council meeting is really appreciable, as the hike of 7% GST would have definitely hit the garment industry hard, and our already low sales would have dropped further had the new rate of 12% GST been imposed on us.”

A taxpayer may be having liquidity issues and as such, not be in a position to make further investments in tax saving instruments. For such taxpayers, there are certain expenditures, which are also eligible for a tax deduction in the financial year 2019-20.

For a taxpayer in India, March is a critical period for ensuring that due taxes have been paid as well as to check that investments, if required, for tax savings have been done. As any delay or shortfall in payment of taxes would result in levy of interest when the tax is paid later on. Not availing of any eligible deductions (sections 80C, 80D etc.), would result in tax, which could have been saved, being paid to the government

In some cases, the taxpayer may be having liquidity issues and as such, not be in a position to make further investments in tax saving instruments. Such taxpayers need not get disheartened as certain expenditures, which they may have incurred and which are also eligible for tax deduction while computing the tax payable to the government can be claimed. In this context, listed below are such expenses which are eligible for tax relief:

1. Children’s education and hostel allowance and tuition fees: Section 10(14) and Section 80C

Any special allowance towards education of children as well as hostel expenditure (generally referred to as Children Education Allowance & Hostel Allowance) granted to an employee by his/her employer is allowed as an exemption under section 10(14) of the Income-tax Act, 1961. The exemption for children’s education allowance and hostel expenditure allowance is restricted to Rs 100 per month and Rs 300 per month, respectively, up to a maximum of two children. Also, section 80C of the Act provides that tuition fees paid to any university, college, school or other educational institution situated in India, for the purpose of full-time education of any two children of the employee is eligible for deduction. Any individual taxpayer (salaried and non-salaried both) can avail of this deduction, if any tuition fee as described above is paid for their children. However, the amount allowable as tuition fees does not include payment in the nature of development fees or donation or capitation fees or payment of similar nature. Further, the deduction is not available if payment is made to a foreign educational institution.

It needs to be noted that children education allowance is different from tuition fees. Children education allowance is available as a deduction only if it forms part of the salary component and the taxpayer has actually incurred expenses towards education of his children. The amount of allowances deductible is Rs 100 per month per child, up to two children. However, in case of tuition fees, it is allowable on the basis of actual expenditure incurred for education of children for maximum up to Rs 1.5 lakh under section 80C, even though the same may not form part of the salary component of taxpayer.

2. Leave Travel Allowance: Section 10(5)

Family vacations or planned destination travelling has become more frequent. Section 10(5) of the Act grants deduction towards the leave travel allowance based on provision of the proof of travel and related expenditure, which are further subject to certain conditions. This deduction can be availed only in respect of maximum two journeys within India in a block of four calendar years. The current block now is 2018-21, which a taxpayer should be aware of. Remember, you must submit the proofs to your employer before March 31, 2020 to be eligible to claim this deduction for FY2019-20

If the travel expenditure related proofs are not submitted to your employer, then you will not be able to claim exemption at the time of filing your income tax return (ITR).

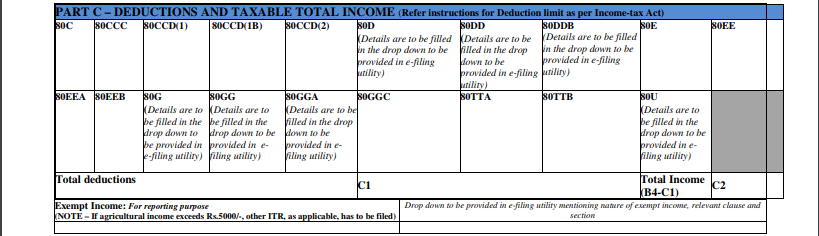

3. Deduction in respect of interest on loan taken for residential house property: (Section 80C, Section 80EE and Section 80EEA)

With the high cost of real estate, a lot of people opt for home loans in order to purchase a house property in their names. Special provision has been carved out for certain first-time homebuyers, wherein the interest component of the equated monthly installments (EMIs) for such a loan can be claimed as a deduction. As per Section 80EE of the Act, an individual taxpayer is allowed a deduction up to a limit of Rs 50,000 for interest paid on a loan taken from a financial institution, sanctioned during the period April 1, 2016 to March 31, 2017 (loan amount not to exceed Rs 35 lakh) for acquisition of a residential house whose value does not exceed Rs 50 lakh. Further, any taxpayer who is not eligible to claim the benefit under Section 80EE of the Act can opt for claiming such benefit under Section 80EEA wherein an individual taxpayer is allowed a deduction up to a limit of Rs 1.5 lakh being paid as interest on a loan taken from a financial institution, sanctioned during the period April 1, 2019 to March 31, 2020 for acquisition of a residential house whose value does not exceed Rs 45 lakh. It is pertinent to note that the above mentioned deductions would not be available to the taxpayer if he owns any other residential house property on the date of sanction of the loan. Moreover, the principal component of the installment can be availed as a deduction under section 80C of the Act and the interest is allowable as a deduction up to Rs 2 lakh in case of self-occupied property

4. Deduction in respect of interest on loan taken for residential house property: (Section 80C, Section 80EE and Section 80EEA)

A deduction every employee should avail the benefit of is the contribution made by the employer under section 80CCD(2) to the notified pension scheme which is not covered within the overall cap of Rs 1.5 lakh for cumulative deductions under sections 80C, 80CCC and 80CCD(1). Under Section 80CCD(2), an employee can get deduction in respect of employer’s contribution towards his National Pension Scheme (NPS) account up to a limit of 10 per cent of his salary. For this purpose, salary includes dearness allowance, if the terms of employment so provide, but excludes all other allowances and perquisites.

The deduction under Section 80CCD(2) of the Act is in addition to the cumulative deduction available under section 80C, where the overall limit is Rs 1.5 lakh, and 80CCD(1B) which is Rs 50,000.

5. House Rent Allowance: Section 10(13A)

House Rent Allowance (HRA) forms a part of the salary in most cases. Many employees who do not own residential house property or stay away from their own residential house property, can avail of the deduction of HRA based on the actual rent paid by them. With respect to HRA, Section 10(13A) of the Act provides for an exemption of least of the following amounts: (i) 40 per cent/50 per cent (in case of metropolitan cities) of the salary amount; (ii) Actual amount received as HRA; (iii) Amount of rent exceeding 10 per cent of the salary

The employee/taxpayer would have to provide the necessary rent receipts/rent agreements and other details to the employer in order to enable the employer to compute the exemption amount. Even if rent receipts are not submitted to the employer, you can claim the tax benefit on rent paid at the time of filing ITR.

6. Employees’ Provident Fund (EPF)

EPF is one of the deductions which is mandatorily made from the salary of most employees and as such, need to be considered while computing the eligible tax deductions. Employees’ contribution towards a recognised provident fund, which is deducted from their salary on a monthly basis, shall be allowable as a deduction under the overall limit of Rs 1.5 lakh under section 80C. No deduction shall be allowable under section 80C with respect to any employees’ contribution towards an unrecognised provident fund.

7. Standard deduction on Salary

The other deduction, which is mandatorily available, is the standard deduction up to Rs 50,000 for all salaried employees. This deduction is considered by the employer while computing tax liability of each employee. This deduction is available at the time of filing ITR. However, while planning your taxes for FY 2019-20, you must consider standard deduction as well to compute your total tax liability.

The government releases the GST return forms details which are mandated to be filed according to the due dates under GST mentioned in the attached notification. The submission and uploading of the returns are totally online. We have mentioned all the GST return filing due dates along with their respective associated GST forms such as GSTR 1, GSTR 3B, GSTR 4, GSTR 5, GSTR 6, GSTR 7, GSTR 8, GSTR 9, GSTR 9A, GSTR 9C in FY 2017-18, FY 2018-19 and FY 2019-20, etc.

GST Calendar of Return Filing Due Dates in March 2020

The government announces GST return filing due dates from time to time in order to maintain taxation in line with respective clearance. Also, the main effort is to alert the taxpayers regarding the GST return filing due dates is to make them neglect any penalty or interest. Here we are offering GST due dates calendar for March 2020 for all the registered taxpayers under indirect tax regime to make them aware of the time period as of when to get their GST return filing done on time.

As GSTR 1 & GSTR 3B is to be filed every month, there is a greater need of getting regular updates/notification based on the GST due dates calendar for avoiding any interest and penalty. Also, there is GST CMP 08 for the composition scheme dealers but it has to be filed every quarter lowering down the need for regular updates on GST due date filing calendar.

GST Return Form Name

Filing Period

Due Dates in March 2020

GSTR 7

Monthly

10th March

GSTR 8

Monthly

10th March

GSTR 1 (T.O. more than 1.5 Crore)

Monthly

11th March

GSTR 6

Monthly

13th March

GSTR 3B

Monthly

INR 5 Crore or More Annual T.O. in the Previous Year – 20th March 2020 for All States/UTs

Less Than INR 5 Crore Annual T.O. in the Previous Year

22nd March 2020 – Chhattisgarh, Madhya Pradesh, Maharashtra, Gujarat, Daman and Diu, Dadra & Nagar Haveli, Karnataka, Goa, Lakshadweep, Kerala, Tamil Nadu, Puducherry, Andaman and Nicobar Islands, Telangana and Andhra Pradesh

24th March 2020 – Jammu and Kashmir, Laddakh, Arunachal Pradesh, Punjab, Himachal Pradesh, Chandigarh, Uttarakhand, Haryana, Delhi, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand and Odisha

GSTR 5

Monthly

20th March

GSTR 5A

Monthly

20th March

Note:

“Extension of due dates for FORM GSTR-3B, GSTR 7 and GSTR 1 for the month of July 2019 to January 2020 till 24th March 2020 for registered persons having principal place of business in the Union territory of Ladakh.” Read Official Press Release

GST Return 1 Due Date (T.O. More Than INR 1.5 Crore)

Period (Monthly)

Last Dates

March 2020

11th April 2020

February 2020

11th March 2020

January 2020

11th February 2020

December 2019

11th January 2020

November 2019

11th December 2019

October 2019

11th November 2019

September 2019

11th October 2019

August 2019

11th September 2019

July 2019

11th August 2019 | Note: “The due date extended till 20th September 2019 for notified districts of Bihar, Gujarat, Karnataka, Kerala, Maharashtra, Odisha, Uttarakhand and also for registered persons whose principal place of business is in J&K.” Notification Here

39th GST Council Meeting – “The requirement of furnishing FORM GSTR-1 for 2019-20 to be waived for taxpayers who could not opt for availing the option of special composition scheme under notification No. 2/2019-Central Tax (Rate) dated 07.03.2019 by filing FORM CMP-02. Extension of due dates for FORM GSTR-1 for the month of July 2019 to January 2020 till 24th March 2020 for registered persons having principal place of business in the Union territory of Ladakh. “Read Official Press Release

The due date of the GSTR 1 form extended till 31st December 2019 for notified districts of Assam, Manipur or Tripura for registered persons. Read Notification

38th GST Council Meeting Important Update: “A taxpayer who has not filed GSTR 1 since July 2017 to November 2019 will not be penalized if they file GSTR 1 by 17th January 2020 (Read Notification). E-way bill for taxpayers who have not filed their FORM GSTR-1 for two tax periods shall be blocked.” Read Press Release & Notification

“Seeks to extend the due date till 20th December 2019 for furnishing of return in FORM GSTR-1 for registered persons in Jammu and Kashmir having aggregate turnover more than 1.5 crore rupees for the month of October 2019.” Read Notification

“Seeks to extend the due date for furnishing of return in FORM GSTR-1 for registered persons in Jammu and Kashmir having aggregate turnover more than 1.5 crore rupees for the months of July 2019 to September 2019 till 20th December 2019”. Read Notification

“The late fee shall be completely waived in case of GSTR-1 for the time period of months/quarters July 2017 to September 2018, which are furnished after 22nd December 2018 but on or before 31st March 2019”

“All the newly migrated taxpayers, a due date extended for furnishing GSTR-1 for the time period of quarterly July 2017 to December 2018 respectively till 31st March 2019”

The filing of GSTR-2 and GSTR-3 has been suspended by the Committee of Officers, which will resume after 30th June 2018. The detailed schedule shall be updated accordingly. The further months of filing for GSTR-1 and GSTR 3B are also decided to be filed till for 6 more months as announced by the GST council meeting.

Penalty of Rs 10,000 will also be imposed on those who don’t link both PAN-Aadhaar card within the deadline.

The deadline to link Aadhaar with PAN has been extended to 31st March 2020 by CBDT, announced the Income Tax Department. According to I-T department, over 30.75 crore Permanent Account Number (PAN) had been linked to Aadhaar till January 27, 2020.

The deadline to link Aadhaar with PAN has been extended to 31st March 2020 by CBDT, announced the Income Tax Department.According to I-T department, over 30.75 crore Permanent Account Number (PAN) had been linked to Aadhaar till January 27, 2020.

Earlier, As per the Central Board of Direct Taxes (CBDT) notification, it was defined that if you did not link your PAN Card with your Aadhaar card by December 30, 2019, your PAN Card will become invalid. However, as per the new rule, if the PAN card and Aadhar are not linked by the end of March 2020 then your PAN will become inoperative from April 1, 2020. Though the government is yet to define what it means by the term ‘inoperative’.

However, do you know how to link your PAN with Aadhaar? Here is a step by step guide which you can follow to link your PAN with Aadhaar. You can check your PAN Aadhaar link online status by visiting the income tax e-filing website www.incometaxindiaefiling.gov.in.If you are already filing tax returns, chances are there that your PAN is already linked with Aadhaar. If you haven’t done, then you need to link.

Here’s how to Link PAN -Aadhaar on Income tax’s website:

Step 2: Go to ‘Link Aadhaar’ option on the left side of the homepage

Step 3: Enter your PAN and Aadhaar number and your name as per AADHAAR

Step 4: Mark ‘I have the only year of birth in Aadhar card,’ if you have only the birth year on the Aadhaar

Step 5: Mark ‘I agree to validate my Aadhar details with UIDAI,’ if you agree to do so

Step 6: Enter the captcha code on your screen

Step 7: Click on ‘Link Aadhaar’ option to request linking of PAN and Aadhaar

Linking PAN with Aadhaar by sending an SMS

The PAN can be linked with the Aadhaar number by sending an SMS to 567678 or 56161 from the registered mobile number. In order to do so, you need to type UIDPAN and send it.

Finance Minister Nirmala Sitharaman, head of Goods and Services Tax (GST) Council, on Saturday announced that the GST Impact on mobile phones will be increased from the current rate of 12% to 18%. The rate is said to be applicable from April 1, 2020. The increase in rates is said to affect the country’s smartphone industry badly. The change will hit the market harder which is already facing a shortage of supplies from China because of the outbreak of Coronavirus.

Mobile phones and specified parts to attract 18% versus 12%. All other items, if there’s a need to calibrate the rates, to remove the inversion, we can take them up in future, examination of that can happen at a later time

GST for maintenance, repair and overhaul service providers in India has been lowered to 5% from 18% now, with provision of availing full input tax credit (ITC). . “This will assist in setting up of MRO services in the country,” the finance minister added. GST rate on handmade and machine-made matchsticks was also rationalised to 12% from present range of 5% and 18%.

“Increase of GST rate on mobile phones to 18%, arguably to correct the inverted duty structure, may lead to increase in prices,” said Pratik Jain, Partner and Leader Indirect Tax, PwC India

“Given the current economic scenario, perhaps an option to provide quicker refund of input tax credit (including on input services which is not allowed currently) could have been explored,”

1. Deferment of the new GST return system and e-invoicing

The implementation of the new GST return system has been postponed to 1st October 2020. Also, the implementation of e-invoicing and the QR code has been deferred to 1st October 2020.

The present return system (GSTR-1, GSTR-2A & GSTR-3B) will be continued until September 2020.

2. Changes in the GST rates

GST on mobile phones and specified parts was increased from 12% to 18%. This decision was taken to avoid difficulties due to the inverted duty structure.

All types of matches have been rationalised to a single GST rate of 12%. Till now, the handmade ones were taxed at 5% and the rest was taxed at 18%.

GST on Maintenance, Repair and Overhaul (MRO) service in respect to aircraft was reduced from 18% to 5% with full ITC.

All these rate changes will come into effect from 01 April 2020.

3. Interest on delayed payments

Now, the interest for delayed GST payment will be calculated on the net tax liability. This amendment will apply retrospectively from 1st July 2017.

4. Extension of GSTR-9 and 9C

The GSTR-9 & 9C deadline is extended to 30 June 2020 for FY 2018-19. Also, the turnover limit will be increased from Rs 2 crore to Rs 5 crore for mandatory annual return filing. Hence, filing GSTR-9C is optional for the taxpayers having the turnover less than Rs 5 crore.

The taxpayers with an aggregate annual turnover of less than Rs 2 crore in FY 2017-18 and FY 2018-19 will not pay any late fee for delayed filing of GSTR-9.

5. Know your supplier

A new scheme called ‘Know your Supplier’ has been introduced so that the taxpayers are informed about the basic details of the suppliers with whom they transact or propose to conduct business.

6. Waiver and extension of due dates

The GSTR-1 for 2019-20 will be waived for certain taxpayers who could not opt for the special composition scheme (notification No. 2/2019-Central Tax (Rate) dated 7th March 2019) by filing Form CMP-02.

The due date of Form GSTR-3B for July 2019 to January 2020 is extended till 24th March 2020 for taxpayers with a principal place of business in the Union Territory of Ladakh. Also, a similar extension is recommended for Form GSTR-1 and Form GSTR-7.

7. Amendment to revocation of cancellation

Taxpayers who have cancelled their GST registration till 14th March 2020 can file an application for revocation of cancellation of registration. The window to fill this application is available till 30th June 2020. The extension is a one-time measurement to facilitate those who want to continue conducting the business.

8. Other decisions

Infosys Chairman, Mr Nandan Nilekani to present progress updates about the GST IT systems at the next three GST Council meetings.

The time limit for finalisation of the e-Wallet scheme for consumers is extended till 31st March 2021.

A special GST procedure was prescribed during the CIRP period for the GST registered corporates who are undergoing insolvency/resolution procedure under IBC Code, 2016.

A transition plan is laid down till 31st May 2020 for the taxpayers belonging to Dadra and Nagar Haveli & Daman and Diu, due to the merger in January 2020.

Refund claims will now be processed in bulk for the benefit of the exporters.

Present IGST and cess exemptions on the imports made under the AA/EPCG/EOU schemes will continue up to 31st March 2021.

1) A decision to defer the applicability of the e-invoicing system

The preparation of e-invoicing seems sub-par, and the GST Council may consider extending the date of implementing the e-invoicing system by three months. It is said that it may be made applicable from 1st July 2020 as against the earlier date of 1st April 2020. With more time at its hands, GSTN may be able to provide improved solutions as well.

2) Rolling out the new GST return system in April 2020

As per the latest development on 7th March 2020, taxpayers are facing many technical difficulties on the GST portal. These have led the GSTN to give Infosys a fortnight to fix them. Given that the government wants to fix the present GST return system sooner, it seems to be looking to stabilise the present system ending in March 2020.

Moreover, the annual GST returns filing facility will be on focus till 31st March 2020. On the other hand, the CBIC and tax officers are increasingly concerned about the number of tax evasions and are looking into the means for its prevention. All these have led to the speculations that the new GST return system might be pushed further by a month or two.

3) The anomaly of the interest charged on delayed GST payment to see an end

The applicability of interest charge is now on the net liability, as opposed to gross liability, but applies prospectively. Many tax professionals and small taxpayers are dissatisfied with the move, requesting the government to make this a retrospective change since July 2017.

4) Relaxing the penal consequences for the notices related to FY 2017-18 and FY 2018-19

There have been multiple instances where the GST notices have been sent out for wrongful tax credit claims and non-payment of interest on delayed GST payment. In some cases, the extended due dates in the previous periods have not been considered while sending out the notices. Considering that the first two years of GST was mostly not stable for taxpayers, giving them relaxations will help them bear less damage. Hence, any penalty or late fees reduction will help them prepare for better compliance in future periods.

5) GST rate structure change and rate hikes speculated

It was speculated in the previous GST Council meeting that the five slab structure would be brought down to three slabs by carrying out a major rate rejig. The 5% tax rate will be hiked up to a maximum of 9-10%, and the 12% tax rate will be removed.

The GST Council has set up a revenue augmentation committee to look into the possible solutions for increasing the GST collections. In addition to these, certain items that were exempted or nil rated may make a comeback under the tax net.

The GST Council has begun correcting the cases of inverted tax structure prevalent for certain items and sectors. In the 38th GST Council meeting, GST on woven and non-woven bags was increased from 12% to 18%. More items such as mobiles, textiles, solar modules, railway locomotives, fertilisers, steel utensils (whose output tax rate ranges between 5-12%) are expected to undergo the rate corrections. However, no major rate changes can be expected in the current scenario.

6) Miscellaneous expected

States will be pushing the centre to resolve the compensation matter, who are most likely to demand full compensation for the fiscal year. Hence, long deliberations are expected in the room. The GST Council will also be discussing the measures to strengthen and build a strong GST system against tax evasions.

The previous GST Council meeting was concluded on 18th December 2019 where an important decision was made to defer GSTR-9 and 9C for the first two years of GST. All eyes are on this GST Council meeting as addressing the taxpayers’ woes tops the agenda.

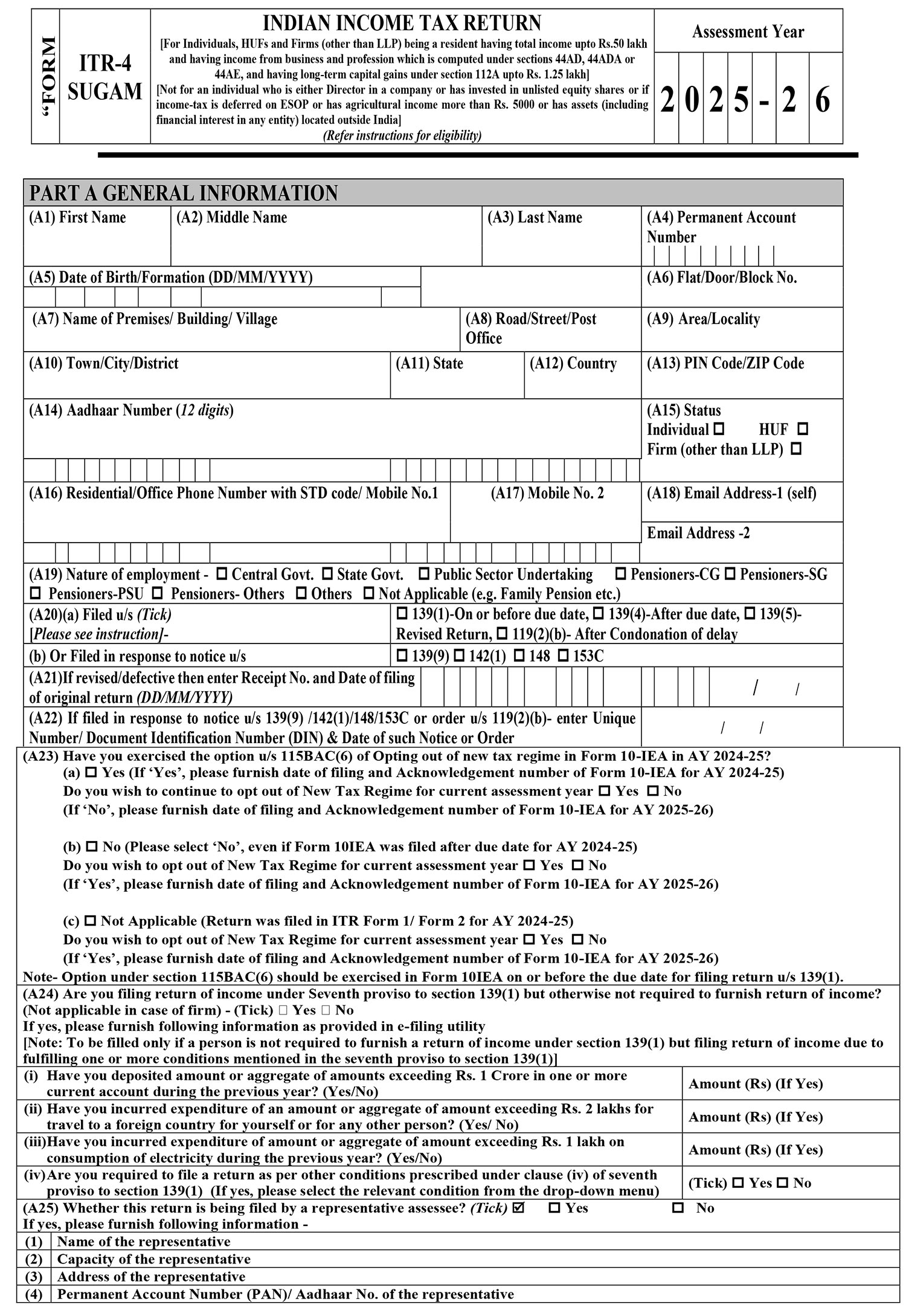

ITR stands for Income Tax Return and ITR 4 Sugam Form is for the taxpayers who are filing return under the presumptive income scheme in Section 44AD, Section 44ADA and Section 44AE of the Income Tax (IT) Act. If the turnover of the aforementioned business becomes more than Rs 2 crores then the taxpayer can’t file ITR-4.

Who can File the ITR 4 Sugam Form?

ITR 4 Sugam form can be filed by the individuals / HUFs / partnership firm(other than LLP) being a resident if :-

Total income does not exceed Rs. 50 lakh.

Assessee having business and profession income under section 44AD,44AE or ADA or or having interest income,family pension etc.

Having agricultural income upto Rs 5,000/-

Have single House property.

It must be noted that the freelancers involved in the above-mentioned profession can also choose this scheme only if their gross receipts are not more than Rs 50 lakhs.

Who can’t File the ITR 4 Form for AY 2020-21?

A person whose income from salary or house property or other sources is more than Rs 50 lakh cannot file ITR 4 Form for AY 2020-21. A person who is a director in a company or has invested in the unlisted equity shares or has any brought forward/ carry forward loss under house property income cannot file the ITR 4 for AY 2020-21.

What are the Major Changes Made in ITR 4 Sugam Form for AY 2020-21?

In Part A, ‘Nature of employment’ section has been deleted.

In Part A, passport details field has been added.

In part A “Are you filing return of income under Seventh proviso to section 139(1) (Not applicable in case of Firm) – (Tick) Yes No . If yes, please furnish following information Have you deposited amount or aggregate of amounts exceeding Rs. 1 Crore in one or more current account during the previous year? (Yes/No) Amount (Rs) (If Yes) Have you incurred expenditure of an amount or aggregate of amount exceeding Rs. 2 lakhs for travel to a foreign country for yourself or for any other person Amount (Rs) (If Yes) Have you incurred expenditure of amount or aggregate of amount exceeding Rs. 1 lakh on consumption of electricity during the previous year? (Yes/No) Amount (Rs) (If Yes) has been added

In part A “whether you are partner or not in a firm” has been inserted.

In Part A Details of partner in the firm (applicable in case of firm) has been inserted.

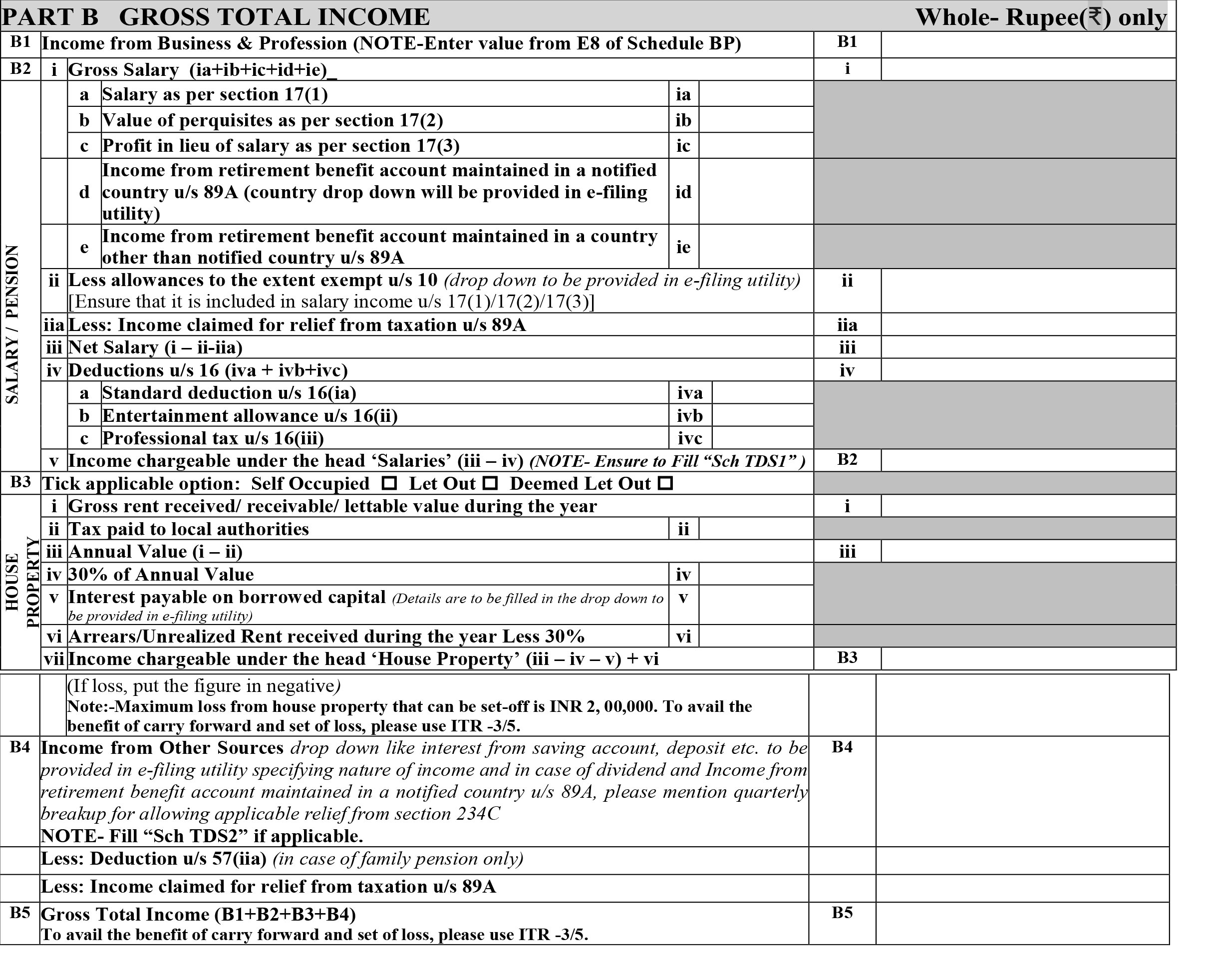

Under salary head details of employer is required to be filed in part B.

Under house property field of “Amount of rent which cannot be realized” has been added.

In other sources head” Deduction u/s. 57(iv) [in case of interest received u/s. 56(2)(viii)]” has been added.

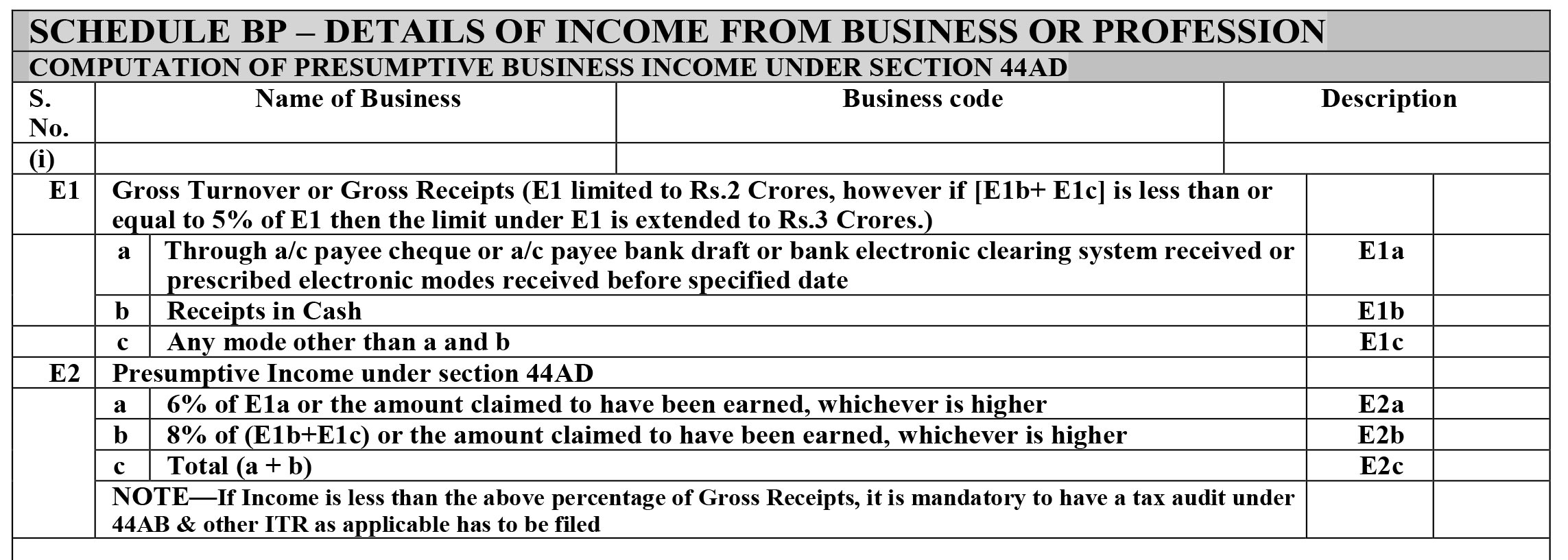

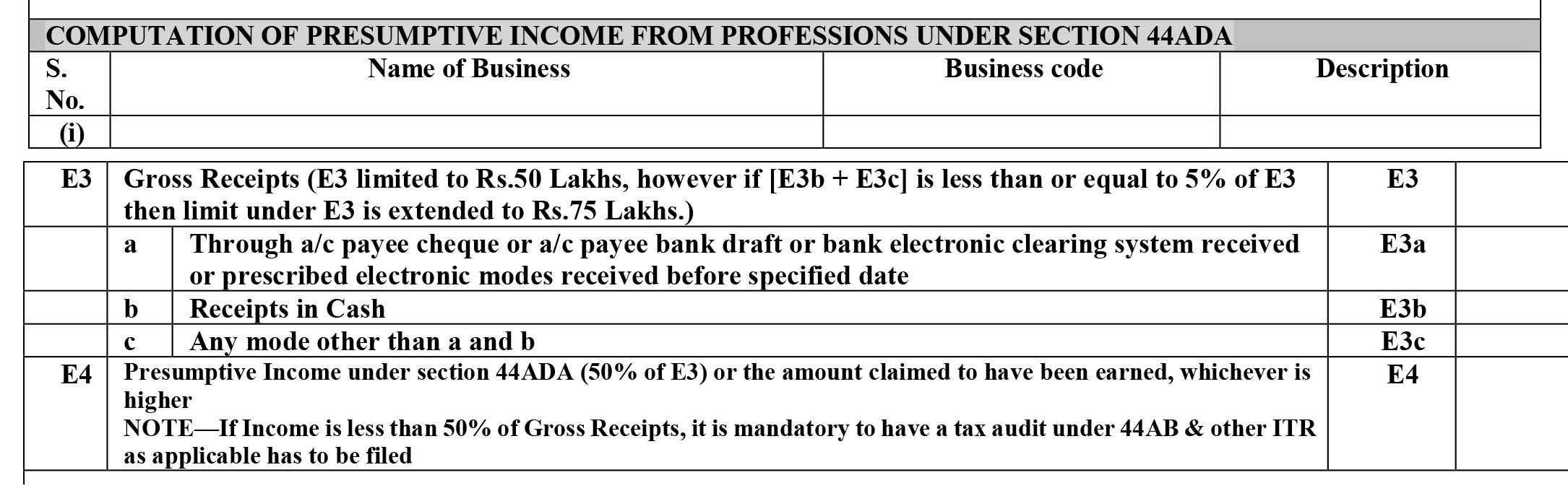

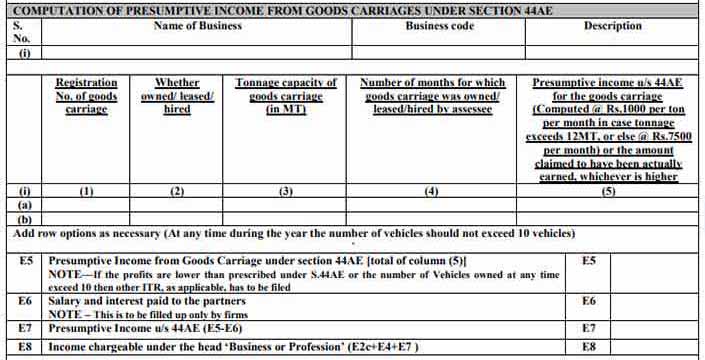

In schedule BP” Changes in table of Gross Turnover or Gross Receipts relatable to presumptive income u/s. 44AE has been inserted.”

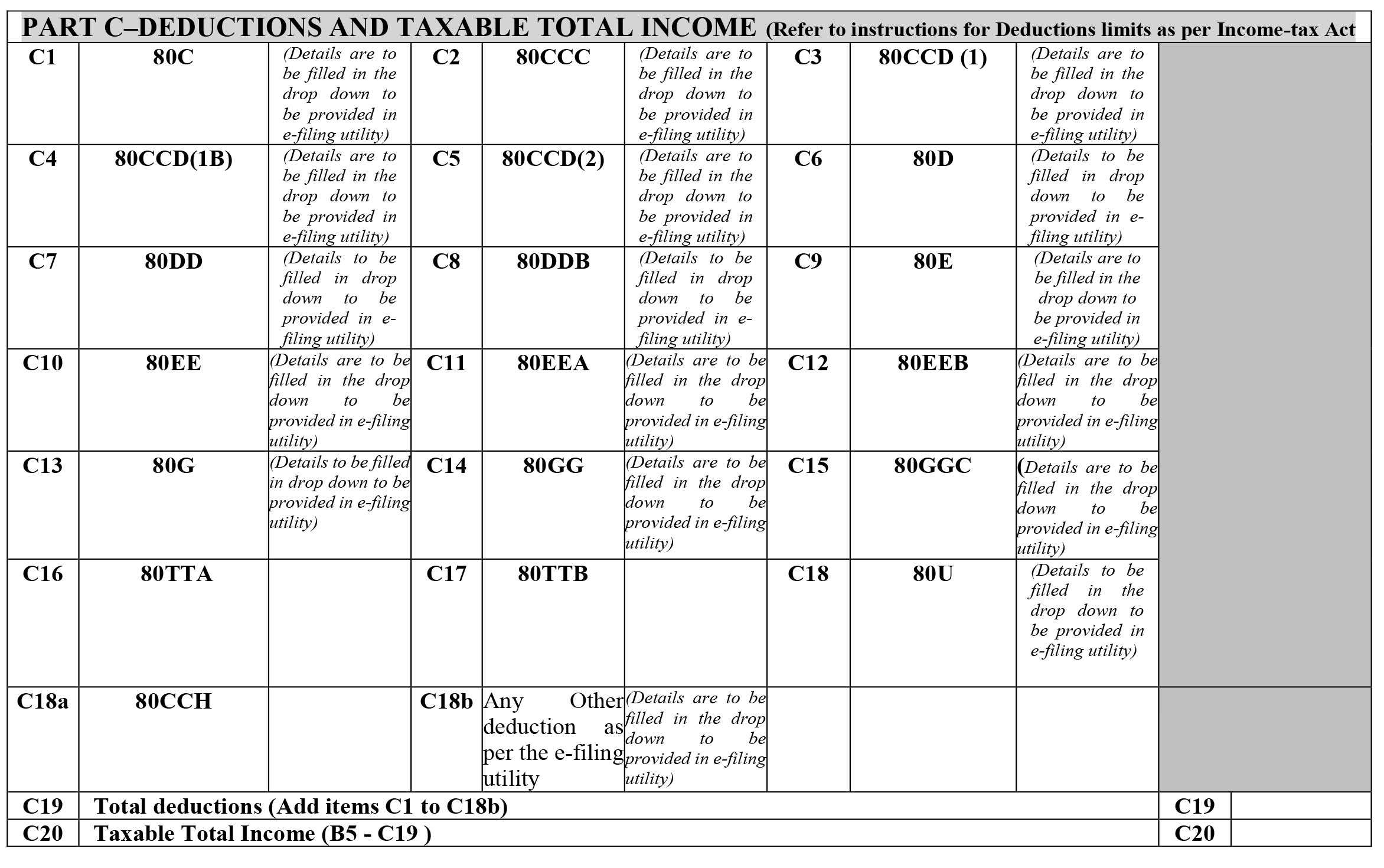

Column of Deduction u/s 80CCGhas been deleted now.

Column of Deduction u/s 80EEA, 80EEB has been inserted.

Schedule 80G has been deleted.

Financial particulars of the business has been deleted.

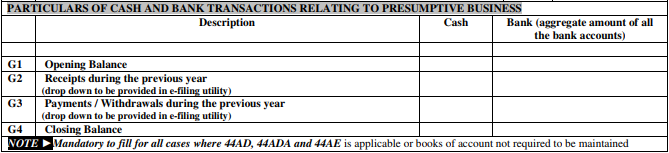

PARTICULARS OF CASH AND BANK TRANSACTIONS RELATING TO PRESUMPTIVE BUSINESS

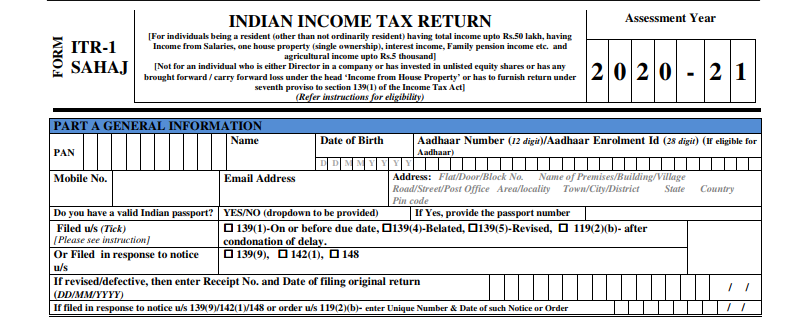

ITR 1 Form is filed by the taxpayers and the individuals being a Resident (other than Not Ordinarily Resident) having Total Income up to INR 50 lakhs, having Income from Salaries, One House Property, Other Sources (Interest etc.), and Agricultural Income up to INR 5 thousand. (Not for an Individual who is either Director in a company or has invested in Unlisted Equity Shares). Also to note down, from now onwards, as mentioned by the tax department, furnishing PAN and Aadhaar card details on the official website of the Income Tax Department is mandatory.

The income tax department has notified ITR forms for taxpayers based on their source of income in order to create a simple tax compliance structure. Therefore, you are required to furnish the return as per the source of your income.

ITR-1 is filed by the taxpayers whose income is up to Rs 50 lakhs from below-mentioned sources:

If the income is from one house property (the case where losses of previous years are carried forward are not included in this ITR)

If the source of income is pension or salary

If the source of income is other sources

If the clubbed income of minor or wife is shown, then ITR-1 can be filed only in case their source of income as mentioned in the above points.

Not Eligible for ITR 1 Filing Online for AY 2020-21

if an individual earns upto Rs 50 lakhs annually, but also have a house, deposited more than Rs 1 crore in a bank account or incurred Rs 200,000 on foreign travel or Rs 100,000 on electricity he/she has to file ITR 4-Sugam form.(Inserted).

Assessee who has to furnish return under 7 th proviso to Section 139(1) of the Income Tax Act (Inserted.)

For the assessment year 2020-21, an individual, or Hindu Undivided Family, which has joint ownership of a house property, cannot file return of income in ITR -1.

Such person will have to file return in ITR-2 or ITR-3, as the case may be.

The taxpayer whose income is more than Rs 50 lakhs is not eligible to furnish this form.

Non-residents and RNOR (Residents not ordinarily resident) cannot file ITR 1.

Taxpayers who have two or more house properties are not eligible.

Assessees having income under business or profession head are not eligible.

Taxpayers who have long or short-term capital gains

Taxpayers whose income from agriculture means is greater than Rs. 5,000

The taxpayer who claims relief for foreign taxes paid or claim double taxation relief as mentioned in section 90/90A/91.

ITR 1 cannot be used by residents having any asset (including financial interest in any entity) located outside India or signing authority in any account located outside India.

Penalty if Miss the Income Tax Return Filing Deadline

As per revised rules under section 234F of IT act from 1st April, 2017 notifies that an individual is liable to pay maximum INR 10,000 penalty after missing the 31st July deadline of ITR filing. While in case an individual total income does not exceed 5 lakhs then a penalty of only INR 1,000 is applicable.

Late Filing Fee Details

E- Filing Date

Total Income Below INR 5,00,000

Total Income Above INR 5,00,000

31st July 2019

INR 0

INR 0

Between 1st August to 31st Dec 2019

INR 1,000

INR 5,000

Between 1st Jan 2020 to 31st March 2020

INR 1,000

INR 10,000

Modifications Details in ITR 1 Sahaj Form

INR 50,000 standard deductions

No applicability on directors of any company

No applicability on individuals holding unlisted equity shares of any company

No changes in computation

ITR 1 & ITR 4 offline availability for senior-most citizens aged more than 80 years

Section wise return filing is segregated within the normal filing return and response to the notice

Salary bifurcation will be done as the standard deduction, entertainment allowance and professional tax

Pensioners column has been added in the nature of employment

Part A General Information requires the details of Valid Indian Passport to be filled by the Assessee.

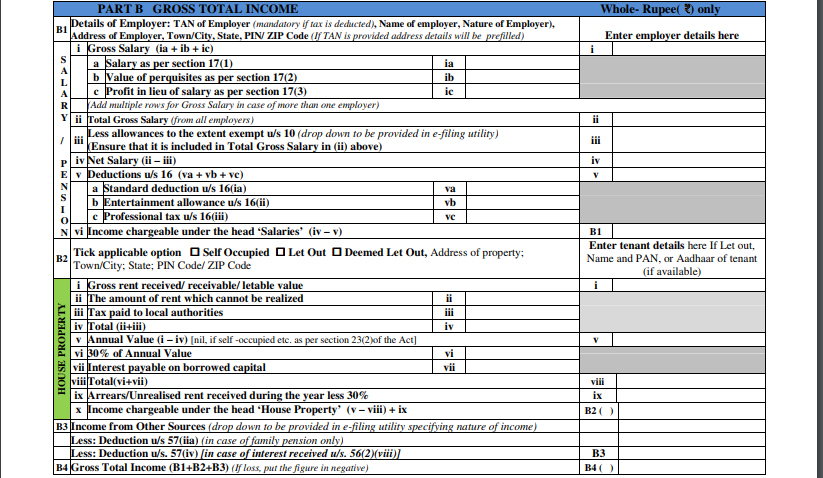

Details of Employer like TAN of Employer (mandatory if tax is deducted), Name of employer, Nature of Employer), Address of Employer, Town/City, State, PIN/ ZIP Code has been inserted under the head income from salary.

Deletion of details of Return of Income filed in response to notice u/s 153A and 153C.

A new deduction of 80CCC,80CCD(1), 80CCD(1B), 80CCD(2), 80DD,80DDB,80E,80EE,80EEA,80EEB,80GG,80GGC,80U has been added in thedeductions column.

A new deduction u/s 57(iv) in case of interest u/s 56(2)(viii) under the head Income from other sources has been inserted.

Point of the amount of rent which cannot be realized has been inserted under the head house property.

The individual income from one house property, salaries and other sources summing up to 50 lakhs, this condition retains its place even after changes

Due Date for Filing ITR 1 Online AY 2020-21

Every year ITR -1 has to be filed on or before 31st July of the following year. After that, a late fee under section 234F is levied

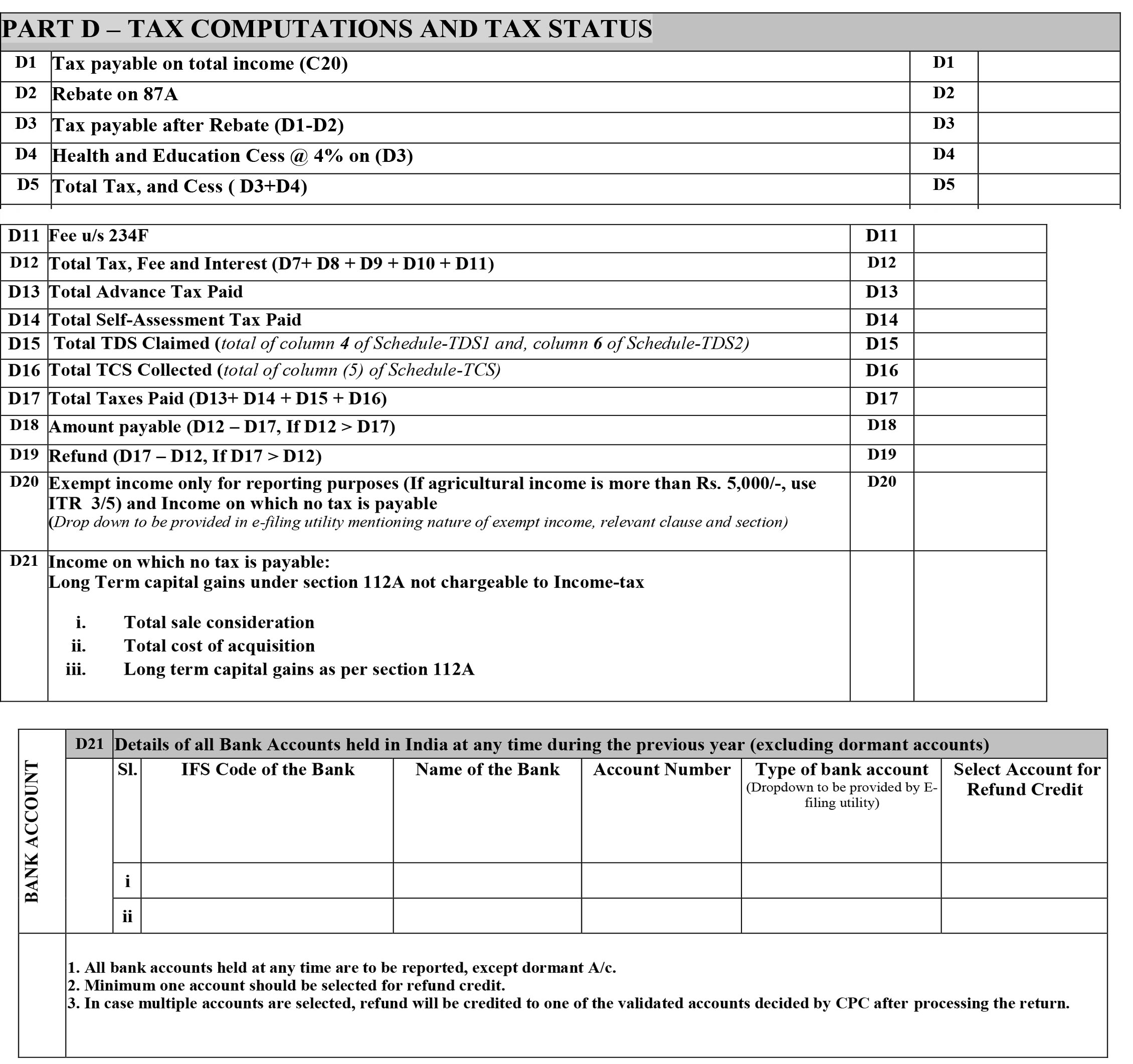

This tab includes all the valuation of tax payable

D1 Tax payable on total income

D2 Rebate u/s 87A

D3 Tax after rebate

D4 Cess on D3

D5 Total tax and cess

D6 Relief u/s 89(1)

D7 Interest u/s 234A

D8 Interest u/s 234B

D9 Interest u/s 234C

D10 Fee u/s 234F

D11 Total tax, fee, and interest

D12 Total tax paid

D13 Amount payable

D14 Refund

Exempt income

Part E – Other Information

This tab includes banking details

IFSC Code of the bank

Name of the bank

Account Number

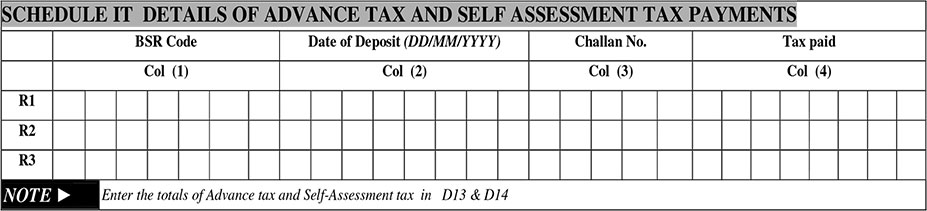

Schedule-IT: IT Details of advance tax and self-assessment tax payments

BSR code

Date of deposit

Serial number of challan

Tax Paid

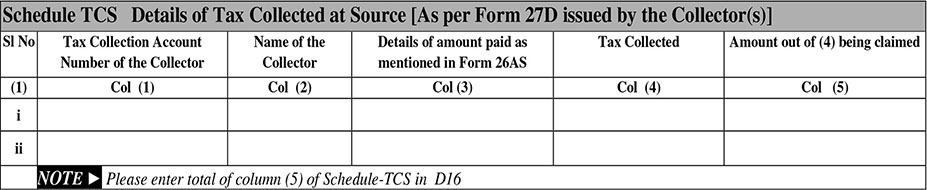

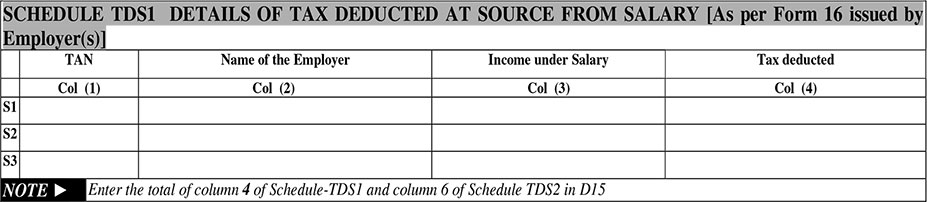

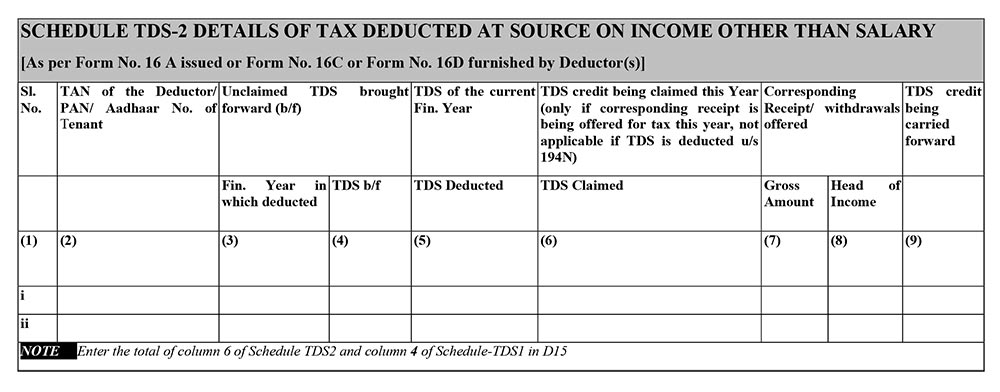

Schedule-TDS: TDS details of TDS/TCS

TAN of deductor/ PAN of tenant

Name of deductor

Gross payment

Year of tax deduction

Tax deducted

TDS/TCS credit

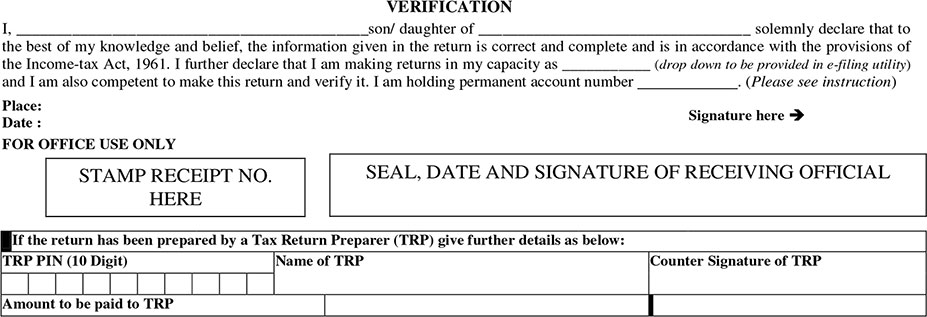

Verification

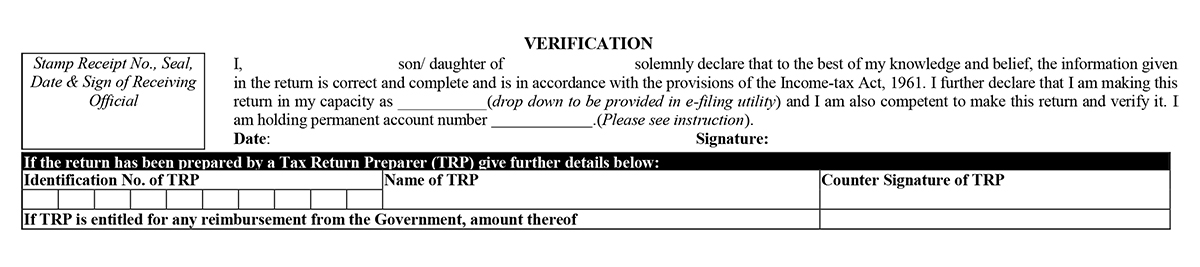

The taxpayer has to verify and self-attest the form at the last by signing the verification content after entering all the details such as name, parent name and PAN details.

Medium To Online Furnish Income Tax Return 1 (ITR)

An ITR-1 form can be furnished either in online or offline mode. In online mode, either XML needs to be uploaded or client can directly login to income tax portal and select the submission mode as “prepare and submit online”. In the case of online filing, some data can be imported from the latest ITR or form 26AS.

Also, super senior citizens (Age of 80 years or more) are exempted from the online filing of ITR.

Offline here means to furnish the return form in paper format.

File ITR 1 Online or Electronically:

While furnishing ITR-1 online, feed the details and e-verify return using EVC via Bank Account/Net Banking/Demat Account/Aadhar OTP or

Feed the details using electronic medium and send a physical copy of ITR V to Centralized Processing Centre (CPC), Bengaluru through speed post or normal post.

When you furnish the ITR-1 return form using electronic medium, the receipt will be seen in the inbox of the registered email id. It can also be downloaded from the official income tax website manually. After downloading the acknowledgement, you need to sign the form and then send to the CPC office, Bangalore before completing 120 days counting from the e-filing date. On the other side, it is not required to send the ITR V to the CPC if EVC/OTP option is used.

File ITR 1 SAHAJ Form Offline

If the age of the person is 80 or more years during the respective tax period or in the previous year.

Important Terms To Understand In ITR-1 SAHAJ Form for AY 2020-21

Notice Number: Notice Number is required to be mentioned when the taxpayer furnishes the return in answer to the notice issued by the Income Tax Department.

Revised Return: There is an option of re-file, so if you have made certain mistakes, you can rectify them again. For the FY 2019-20 the taxpayer can furnish the revised return on or before 31 March 2021.

Advance Tax: If the tax on other income is above Rs. 10,000 in a year, the assessee is required to calculate and deposit the advance tax. This advance tax is to be paid on a quarterly basis such as on, June, December, September and March.

Annexure-less Return: Annexure-less return which means it doesn’t require to affix any documents with the ITR-1 Form.

Let’s Go Through ITR-1 Return Filing FAQ’s

Q.1 What documents one needs to submit while filing tax returns?

No document is needed to be submitted while filing income tax returns. However, one should keep basic documents like Form 16, balance sheet and P and L accounts of the business, shreds of investment evidence, audit reports and so on ready with him/herself. Because in some cases when the income tax department sends notice, these documents are required to be presented before the tax authorities on a later date.

Q.2 – What are the heads under which Pension and family pension are taxable?

Income from salary’ is the head for levying a tax on pension whereas family pension is taxable under the head ‘Income from other sources.

Q.3 – Who is eligible to file return via paper form rather than e-filing an ITR?

YEvery income tax assessee has to mandatorily e-file income tax returns. However, there are some exceptions to the standard rule wherein they can submit paper ITR forms and they do not have to file the ITRs online. They are as follows:

At present, Super senior citizens who are above 80 years of age.

Q.4 – What amount will attract tax if the value of the gift is more than Rs. 50,000?

When the value of the gifts received from friends on any event except the wedding during a year is Rs 50,000 then the whole amount will attract tax under the head ‘Income from Other Sources’ head.

Note: Gifts are taxed on the total value of all the gifts received in the year and not on the value of the individual gifts.

Q.5 How bank accounts are reported in ITR-1?

Details of savings and current accounts which are held during any time of the previous year must be reported in Part E of the ITR form which seeks – other information. The account number must comply with the Bank’s Core Banking Solution (CBS) system. However, one need not provide details of dormant accounts which is not working since 3 years.

Q.6 – Can ITR-1 be filed in case of exempt agricultural income?

Yes, one can file ITR-1 when the agricultural income is not more than Rs 5000. But when it exceeds Rs 5000, one needs to file ITR 2.

Q.7 – Is it necessary to file an ITR if the annual income does not exceed Rs 250,000?

No, it is not necessary to file an ITR if the annual income is less than Rs 250,000. But in this case, a ‘Nil Return’ should be filed to upkeep a record which is an employment proof required while applying for a passport or loan.

Q.8 – Does dividend income from Mutual Funds need to be included in it?

Yes, dividend income from mutual funds should be included under the head ‘Exempt Income(others)’ as it is an exempt income u/s 10(35).

Q.9 – Can I file ITR-1 if I have a House Property loan?

Yes, you can file ITR-1 if you have a house property loan.

Q.10 – Should I file ITR-2 or ITR-1, if my maximum exempt income is more than Rs. 5,000? What much amount of income will be considered as exempt income?

ITR-2 has to be filed if the amount of aggregate exempted income is more than Rs. 5,000. Some incomes are tax exempt as per Section 10 of the Income Tax Act. A few examples of exempt income are as follows:

Income from Agriculture

Long term capital gain on listed shares and securities (Section 10(38)

Gratuity, Pension and Leave encashment are exempt u/s 10 of the Income Tax Act.

Maturity amount of LIC (Section 10 (10D)

Q.11 – Can I file ITR-1 if I have a Rental Income?

Yes, you can file ITR-1 if you have a rental income. Refer our guide for the step-by-step process.

Q.12 – Should Interest Income be mentioned under the head ‘Income from Other Sources ‘ while filing ITR-1 when TDS has already been subtracted?

Yes, Interest Income should always be mentioned under the head ‘Income from Other Sources’ even when tax has already been subtracted by the bank.

Q.13 – Do I still need to furnish my Bank Account details in the ITR if there is no refund due to me?

Yes, furnishing the bank details in the ITR is mandatory, regardless of refund is due or not. It is mandatory because many taxpayers pay more taxes than their tax liability. So, to enable the Income Tax Department to send refunds on time, bank account details need to be furnished.

Q.14 – How can I download the Income Tax Return Form?

Income tax return forms are available on the official website of the Income Tax Department. Simple steps to download forms are as follows:

Go to the Income Tax Department website

Click the option ‘Form/Downloads’ on the homepage.

Choose the option of ‘Income Tax Returns’ from the drop-down menu.

Now you will be redirected to the ‘Income Tax Return’ webpage. Now download the form which is appropriate according to your source of income and A.Y.

Q.15 – What is the meaning of ITR XML file?

ITR XML is a kind of file format which is generated when you file the important data of your ITR in an offline utility.

Currently introduced by FM Nirmala Sitharaman, Union Budget 2020-21 seems to be a set of challenging income tax provisions. There have been no provisions like the provisions of Union Budget 2020. In the said budget, FM has introduced the new tax slabs with reduced slab rate which taxpayers may adopt on a voluntary basis. This means taxpayers have a choice of selecting either of the two options (old or new slabs rate). It is witnessed that the new slabs are not much in favor of the employed individuals and adopting the new income tax slab 2020 might lead them to a huge tax outgo from their accounts.

Government Vision

According to CA Vinod Jain, the administration is now looking forward to having a simplified version of the tax rate structure and also the normal taxpayers who have no investments should get some incentives. Earlier when the corporate sector enjoyed a considerable benefit in tax rates there was an echo seeking incentives for the common taxpayers.

According to him, the new tax rates FY 2020 are not beneficial for the employed individuals who have their investments in the form of PF, insurance, home loans, etc. LTA, house rent, standard deduction, medical such as 80 C, investment of Rs 2 lakh, etc. are non-exempt as per the protocols of the new Union Budget.

Read Also: Current Income Tax Rates for FY 2019-20 (AY 2020-21)

Example: Here if a taxpayer is not having enough investments then it is beneficial for him to go with the new slab and later on if he invests in multiple instruments then he can switch back to the old tax slab.

As declared by Manish Khemka (chairman of Global Taxpayers Association and co-chairman of the PHD Chamber of Commerce and Industry-UP), the amendments in the tax slabs are actually a step towards the future direction. The government is aiming towards an entire simplified new GST system and so the complexities related to various concessions are over.

Next, there will be a system where the tax rates will be less and there will be more incentives on the investments. The step will allure the new professionals with high packages to invest. Such professionals are heavily taxed and therefore FM Nirmala Sitharaman has given them the relief in Budget 2020.

Drawbacks

Several employed individuals have already invested in LTA, PF, home loan, life insurance, etc. and every single year a considerable amount from their bank balance goes in such instruments. So clearly such salaried individuals will want to stick to the old tax slabs fy 2019-20 rather than shifting to the new slabs fy 2020-21.

As per Tax Expert Balwant Jain, many incentives in terms of tax payment have been abolished which makes it a less attractive choice of the taxpayers. According to him, a regular taxpayer will have to hire a tax expert to know the profit and loss arising after the deductions and exemptions as per the new policies.

Nobody is ever going to sacrifice the handsome amount earned under the exemption in the old system. There is no one who is not availing the benefits of exemptions under 80C. The old system had the standard deduction up to Rs. 50,000, LTA, interest on a home loan, Rs 50,000 on interest income to senior citizens, which no taxpayer would want to give up for the sake of adopting the new policies.

Below is the study revealing the advantages and disadvantages of both the system under different salaries:

Salary Rs. 10 Lakh Per Annum

Old Tax Slab FY 2019-20

If a professional with an annual package of Rs. 10 Lakhs has no investments, then such a person is compelled to pay the total tax of Rs. 1,12,500 as per the old slabs.

Deduction – From the above-mentioned amount Rs. 50,000 is reduced as the standard deduction, now he is obliged of paying Rs. 1.5 lakhs under 80C, 25,000 under mediclaim and 2 Lakh interest a year for a home loan. So clearly his payable tax is just Rs. 27,500.

New Tax Slabs for FY 2020-21

As per the new tax slab, the overall taxability of the person with an income of Rs. 10 Lakh per annum is Rs. 75,000. If an individual adopts the new tax slab then he/she is in a loss of Rs. 47,500 in a year.

Salary Rs. 12.5 Lakhs Per Annum

Old Tax Slab FY 2019-20

As per the old tax slab if the standard deduction is excluded (that means he/she has not done any investment) his total payable tax is Rs. 1,87,500. If the standard deduction is included then Rs. 50,000 is reduced from the tax-ability of the person. And if he has paid Rs. 1.5 lakh under 80C, Rs. 25,000 under Mediclaim and an interest of Rs. 2 lakh on a home loan in that year. Then his total taxability remains Rs. 77,500 only.

New Tax Slabs for FY 2020-21

As per the new tax slabs rate 2020, an individual with a gross income of Rs. 12.5 lakhs per year is liable to pay Rs. 1,25,000 as tax. So the individual adopting the new tax slab is clearly in the loss of Rs. 47,500.

Important: Section-Based Income Tax-Saving Tips For Salaried Person

Salary Rs. 15 Lakhs Per Annum

Old Tax Slab FY 2019-20

If a salaried individual with an annual income of Rs. 15 Lakhs is not having any investment and the standard deduction is also excluded then his/her total tax liability is Rs. 2,62,500. On the other hand if the standard deduction of Rs. 50,000 is excluded and if he has paid Rs. 1.5 lakh under 80C, Rs. 25,000 under Mediclaim and an interest of Rs. 2 lakh on a home loan in that year then his/her total tax liability falls down to be only Rs. 1,35,000.

New Tax Slabs for FY 2020-21

As per the new income tax slabs 2020, an individual with a gross income of Rs. 15 lakhs per year is liable to pay Rs. 1,87,500 as tax. So the individual adopting the new tax slab is clearly in the loss of Rs. 52,500.