A taxpayer is going to receive the advantage of the rebate if the taxable income calculated after the eligible tax exemptions and deductions results to be less than INR 5 Lakhs. Under the current provisions of the Income Tax Department, a taxpayer can enjoy a maximum rebate of INR 12,500 under section 87A of the Income Tax Act if he/she has a taxable income less than INR 5 Lakhs.

However, if the taxable income goes up by as low as INR 1, then you will be revoked from securing the rebate and will be obliged to pay the taxes according to the tax-slabs and provisions of the Income Tax Act Get to know complete guide of TDS provisions under income tax act 1961 at here. Also, we include several topics as TDS returns, TDS due dates, penalty & more. Read More .

The taxpayers having a taxable income of more than 5 Lakhs will be paying the taxes on an income more than the difference by which their income is going up by 5 Lakhs.

Let’s Take An Example to Understand This:

Suppose your taxable income calculated by your CA is INR 5,10,000. Then your tax liability arising will be:

| Income | Tax Liability |

|---|---|

| Up to Rs 2.5 lakh | 0 |

| Between Rs 2.5 lakh and Rs 5 lakh | 5% of Rs 2.5 lakh = Rs 12,500 |

| Income above Rs 5 lakh (Rs 10,000) | 20% of Rs 10,000 = Rs 2000 |

| Total tax liability | Rs 14,500 |

| Final Tax liability with cess @ 4% | Rs 15,080 |

From the above table, it is clear that if the taxable income of an individual is below INR 5 Lakh he/she will be getting a rebate of INR 12,500 but as soon as his income goes above INR 5 Lakhs then he will have to pay tax on the difference amount at the rate 20% along with the earlier rebated amount of INR 12,500.

The taxpayer is said to have paid higher, as he would have faced the tax on the difference amount of INR 10,000 at the rate of 20%, instead, he has to bear the burden of INR 15,080, inclusive of the rebate, which is even higher than the difference amount (15,080>10,000).

As a result of this, the taxpayer will be left with an income to spare of INR 4,94,920 (5,10,000 – 15,080) instead of the earlier amount he would have been getting after rebate, that is, INR 5,00,000.

Now, if the said person would have donated the excessive amount of INR 10,000 to an organization where he will get 100% deduction under Section 80G or any other section, this would have resulted in him having a more income in his hand.

A CA in a statement said that a person is likely to pay more tax if the income exceeds INR 5 Lakhs. That means the individual would be wound up paying a tax on a bigger amount then the difference amount. Moreover, the individual will not be getting the benefit of Marginal relief unlike that in the case when the income crosses INR 50 Lakh, INR 1 Crore, etc. depending on the cases.

In the case of Marginal Relief, an individual is relieved from the tax due to the crossing of a tax slab rateGet the details on income tax rates for FY 2019-20 (AY 2020-21). Various rates are provided such as Individual/HUF, Companies, Partnership Firms. Read More. The motive is to save an individual from paying the tax at the rate of the amount from which the income is exceeding.

What is the solution to this problem?

The best solution, in this case, is to avail the benefit of various deductions from the Income Tax Act, namely under 80C, 80D, etc. You just have to contact your CA who will inform you about these deductions in detail. You can also avail the deduction under 80G, by donating some amount, in case all the other deductions have already been used. But before donating you should check how much deductions will you be getting as there are different deduction rates for different organizations.

Get to know about GST E Way bill and its generating process through online and SMS in a simple manner. Also, we have attached original screenshots of official E way bill portal for better understanding

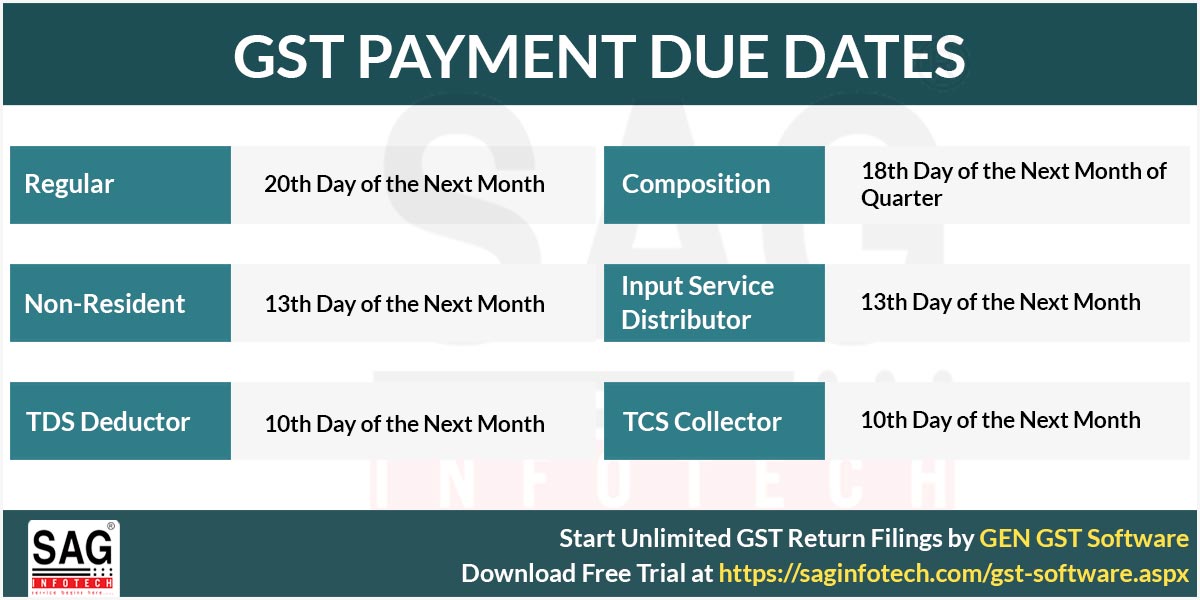

Get to know about GST E Way bill and its generating process through online and SMS in a simple manner. Also, we have attached original screenshots of official E way bill portal for better understanding Check out due dates of payment under GST for general and composition taxpayers in India. We have included penalty charges on late payment with interest

Check out due dates of payment under GST for general and composition taxpayers in India. We have included penalty charges on late payment with interest